Announcements

Drinks

Reber Acar

Analyst

Karlo Fuchs

Team leader

Keith Mullin

Press contact

Germany: systemic risk buffer well intended but won’t stop problems emerging

By Reber Acar, Associate Director, Covered Bonds

By Reber Acar, Associate Director, Covered Bonds

In and of itself, the systemic risk buffer will have a limited impact. In fact, its broad-based nature could even cause collateral damage. Capital-based measures are only designed to increase the resilience of the banking system after risks have already emerged. For now, the little differentiation that the systemic risk buffer provides could do more harm than good as it targets a banks’ whole mortgage businesses, including prudently underwritten lending.

Mortgage financing is required to bring the German home ownership rate of 51% closer to the 70% European average, and of course for the mammoth task of greening the housing sector. As such, criticisms from the German Banking Industry Committee (Deutsche Kreditwirtschaft), the umbrella group representing Germany’s five leading banking associations, is understandable.

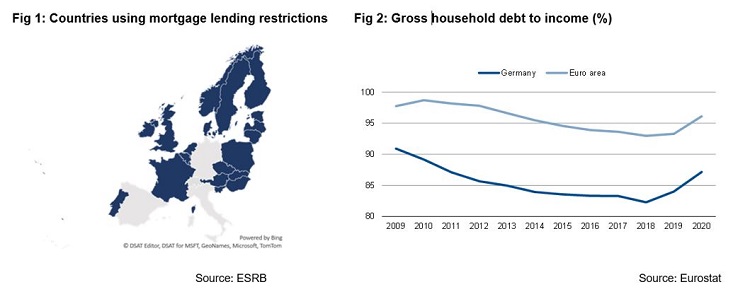

As far back as 2017, Bafin stated that that the impact on mortgage lending because of changing prices would be minor. To prevent risks emerging and adequately ensure financial stability requires direct borrower-based macroprudential measures. Rather than ensuring you are covered when a loan has defaulted (using higher risk buffers) it is better to avoid the risk emerging in the first place; a strategy most other European regulators actively use (see Figure 1).

Macroprudential measures should directly limit mortgage lending to the riskiest borrowers i.e. borrowers combining high LTVs, low amortisation and low debt-service capacity. Effectively, such measures represent minimum standards for prudential mortgage lending. It comes therefore as no surprise that in its renewed warning last Friday, the European Systemic Risk Board is not only recommending LTV limits but income-based measures too.

The Bundesbank, however, believes that borrower-based macroprudential measures represent material interference in contractual freedom. This is especially true for LTV limits. A hard LTV limit of 80%, for example, would exclude a significant portion of middle-income German households from purchasing their own homes, which could lead to socials tensions certainly not desired by policy makers.

As such, interference would need to be backed by solid data; data that the German regulator may not have until mid-2023 (see our comment: Bundesbank takes wait-and-see approach while house prices increase at record pace). It appears that legal rather than financial stability considerations are preventing the German regulator from using these tools.

Currently, low home ownership rates explain why German household indebtedness is well below the European average (see Figure 2 above). Fuelled by increasing prices, this has changed significantly, however. We believe the activation of a less intrusive and more flexible amortisation requirement, complemented by a debt-to-income measure (best tested with an additional interest-rate hike) is justified. Over-valuations and an increasing debt-fuelled house-price boom need to be addressed to avoid financial stability risk. A continuation of the wait-and-see mode to mid-2023 when granular lending data is finally available is dangerous. Even more so as measures only will impact new lending and take time to become effective. Measures should be activated now.

Reber Acar

Analyst

Karlo Fuchs

Team leader

Keith Mullin

Press contact