Announcements

Drinks

Florent Albert

Analyst

Chirag Shekhar

Analyst

Shan Jiang

Analyst

David Bergman

Team leader

Keith Mullin

Press contact

European CMBS Outlook and H2 2021 update: primary market set for all-time record

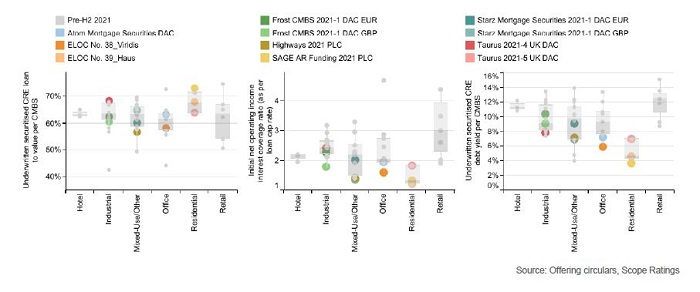

Eight CMBS and one CRE CLO priced in the second half of last year for EUR 3.2bn, pushing full-year issuance to EUR 5.8bn; surpassing our EUR 5bn forecast. Transactions exhibited all-time low cashflow metrics, driven by residential and industrial CMBS; and the further optimisation of junior investment-grade notes.

“Lenders financing residential and industrial assets took advantage of the resilience and attractiveness of these asset classes to achieve attractive refinancing through CMBS,” said Florent Albert, director in Scope’s structured finance team in a report out today.

In terms of the key themes of H2 primary flow, beds and sheds continue in favour, with two residential and one logistics CMBS. “Issuance of office deals continued, although investor cautiousness around single-office asset transactions is growing, particularly when assets have high vacancy rates,” said Benjamin Bouchet, a director in Scope’s structured finance team and co-author of today’s report.

Geographic diversification also continued, with one transaction backed by German multifamily assets. Five multi-jurisdiction CMBS emerged in 2021, more than the whole of the previous three years, demonstrating the internationalisation of this historically UK-focused product.

ESG-friendly CMBS were sought after; one transaction featuring a BREEAM excellent rating and another a securitisation of social housing. Asset-type diversification continued too, with one UK deal backed by motorway service area assets and another a cold-storage properties deal.

On the structural front, new developments included a dual currency issue and the first ever European CRE CLO. “It highlights market maturity and increasing investor confidence in European CMBS and in asset classes that have a proven track record in the US, like cold storage or CRE CLOs,“ said Albert. Also, the share of CMBS with no scheduled principal amortisation, excess spread leakage and modified pro-rata priority of payments has become the norm, resulting in higher volatility in the credit profile of CMBS notes.

“Credit metrics in deals that came in the second half of the year were more aggressive than in the first half and in previous years. Interest Coverage Ratios and debt yields hit an all-time low; a trend exemplified in multi-family and social housing CMBS,” said Shan Jiang, associate director in Scope’s structured finance team and co-author of today’s report. “Higher refinancing leverage for industrial assets and lower rental income for office transactions also contributed to the trend to lower debt yields.”

CMBS credit metrics per asset type : H2 2021 vs. H1 2018-H1 2021 issuance

The CMBS Outlook and H2 update is available for download here. This publication forms part of Scope’s monitoring of the European CMBS market and is the latest is a series of CMBS-focused publications. To access our two-part European CMBS research series from 2021 and watch our Webinar on the revival of the European CMBS market, see here.

Access all Scope rating & research reports on ScopeOne, Scope’s digital marketplace, which includes API solutions such as for Credit Sphere.

Florent Albert

Analyst

Chirag Shekhar

Analyst

Shan Jiang

Analyst

David Bergman

Team leader

Keith Mullin

Press contact