Announcements

Drinks

Florent Albert

Analyst

David Bergman

Team leader

Keith Mullin

Press contact

A primer on European CRE CLOs: same foundations as US CRE CLOs. Same success?

CRE CLOs are securitisations of loan portfolios secured by transitional commercial real estate. They are an evolution of CMBS and the two products share many elements, although CRE CLOs provide more flexibility, alignment of interests and structural enhancements.

“CRE CLOs are used primarily to provide CRE CLO sponsors with non-mark-to-market, non-recourse term financing alternatives to traditional warehouse lines or repo facilities,” said Florent Albert, a director in Scope’s structured finance team and author of a CRE CLO primer out today. “They are not a pure spread arbitrage product like CMBS. They are a match term-funding balance-sheet solution for lenders to refinance their short-to-medium-term floating-rate loan portfolios on attractive conditions.”

The macro environment supports the development of a European CRE CLO market. “The continuous growth of non-bank CRE lenders, the recent re-emergence of European CRE capital markets, capital needs to address ESG and Covid-19 impacts, the inflationary environment as well as investor appetite for non-traditional forms of collateral with a yield premium are all drivers of growth for a European CRE CLO market,” Albert continued.

Unlike in the US, banks have financed the majority of European CRE. But the global financial crisis, tighter banking regulations and increasing capital requirements led to banks exiting regulatory capital-intensive sectors like real estate (re)development and created a competitive advantage for alternative lenders, which benefited from favourable regulatory treatment.

Alternative lenders like insurance companies, private equity funds and debt funds have gained momentum and massively grown their CRE lending balance sheets. “They are now seeking alternative sources of financing to scale up their CRE debt platforms. CRE CLOs offers many benefits compared to warehouse lines, bank loans or corporate debt,” said Albert.

CRE CLO sponsors are positive about recent developments in Europe’s CRE capital markets as an alternative to the traditional banking sector. The entry of large US non-bank lenders in the aftermath of the global financial crisis changed the environment for CRE lending. US non-bank players have the capacity, expertise and willingness to tap the capital markets to gain more competitive advance rates, a cheaper cost of funds and more discretion around asset selection, as they do in the US.

Investors, meanwhile, like the alignment of interest in CRE CLOs, where transaction sponsors remain heavily incentivised via retention of junior tranches and structural senior note protection cutting off cash flow to equity in case of under-performance.

Properties underlying CRE CLOs are generally composed of major CRE asset types. “But properties are considered as transitional and riskier than CMBS secured stabilised assets and are exposed to a number of credit risks, including redevelopment/repositioning or lease-up risks; business plan risks; and exit strategy risks,” Albert said.

CRE CLOs can be static or managed, with reinvestment and ramp-up periods, and allow for performing loan modifications and repurchase of defaulted or credit risk loans. They also embed interest coverage and over-collateralisation note protection tests.

The development of the European CRE CLO market also faces challenges. “The main hurdles lie with country-based CRE laws and regulations, multiple currencies and European-based securitisation standards. Tenant evictions laws, planning regulations, and requirements or enforcement laws differ widely from one country to another and European grace periods are shorter than US ones,” Albert said.

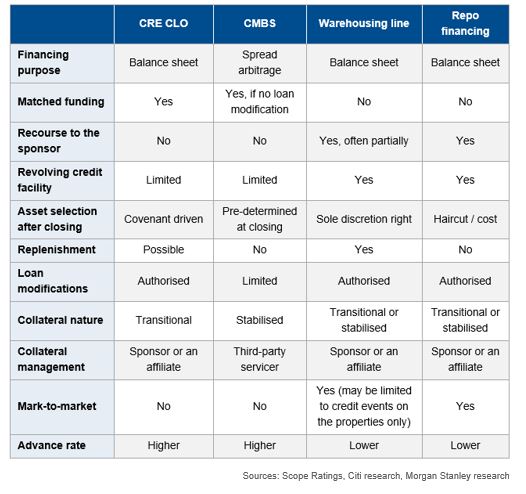

Comparison of CRE funding schemes

Download Scope’s Primer on CRE CLOs here.

Access all Scope rating & research reports on ScopeOne, Scope’s digital marketplace, which includes API solutions such as for Credit Sphere.

Florent Albert

Analyst

David Bergman

Team leader

Keith Mullin

Press contact