Announcements

Drinks

Thomas Gillet

Analyst

Alvise Lennkh-Yunus

Team leader

Matthew Curtin

Press contact

Egypt: devaluation, financial support mitigate near-term risks, but challenges remain

By Thomas Gillet and Tom Giudice, Sovereign and Public Sector Ratings

Although additional support from international partners mitigates financing pressures, addressing durably Egypt’s (B-/Negative) external-sector resilience and financing constraints requires more progress in meeting conditions for continued IMF support. Priorities for the Egyptian authorities are setting up a credible, flexible exchange-rate regime, adopting tighter monetary and fiscal policies, and creating a business environment more conducive to private-sector activity.

The scale of bilateral financial support that Egypt has received from the United Arab Emirates (UAE) will ease near-term tensions on the country’s balance of payments. The upfront investment by the Abu Dhabi Developmental Holding Co. (ADQ) is worth USD 35bn, or about 9% of 2023 GDP.

The move enabled the Central Bank of Egypt to undertake a long-overdue devaluation of the pound (from EGP 31 to EGP 48 per USD presently), allowing for the unification of the official and unofficial exchange rates. The devaluation has paved the way for an increase in the IMF Extended Fund Facility (from USD 3bn to about USD 8bn) and additional support from the European Union (EUR 7.4bn) as well as the World Bank (USD 3bn).

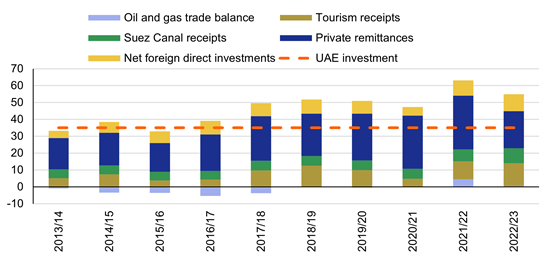

This financial support is large relative to Egypt’s gross external financing needs, estimated around USD 20bn per year on average over 2024-25 and the long-term deposits made by Gulf countries at the Egyptian central bank of around USD 15bn. Financial support is also significant in the context of regular external financing sources, mostly remittances inflows (USD 24bn a year on average between fiscal years 2013/14 and 2022/23), tourism-sector receipts (USD 8bn) and Suez Canal receipts (USD 6bn; Figure 1).

Figure 1. UAE’s investment is large relative to Egypt’s regular foreign-currency inflows

USD bn, per fiscal year (July-June)

Source: Central Bank of Egypt, Scope Ratings

Boosting long-term external resilience conditional on exchange-rate flexibility

However, recent financial support packages from bilateral and multilateral partners will enhance Egypt’s resilience to external shocks in the long run only if supplemented by further reforms to improve the business environment. This should enable more official-sector disbursements as part of the IMF programme and a gradual replenishment of net international reserves (USD 35.3bn as of end-February) driven by foreign direct investment rather than by international financial support.

The authorities expect that the ADQ investment will be a catalyst for up to USD 150bn in additional foreign direct investment in the coming years. Reaching such an ambitious target would require the government to create the conditions for private-sector-led GDP growth, beyond the recent elimination of the preferential tax treatment and exemptions for state-owned enterprises.

One crucial aspect for significantly raising foreign investment inflows will be the Central Bank of Egypt’s ability to maintain a more flexible inflation-targeting regime allowing market forces to set the exchange rate. The uneven policy-making environment since October 2022, suggests that this process may not be smooth, with limited fluctuations of the pound since the devaluation on March 6 suggesting central-bank interventions in currency markets.

If the authorities aim only to continue managing the value of the pound at lower levels instead of allowing the currency to fully float, this may fall short of IMF conditions for future disbursements and complicate cooperation with the official sector. For now, international partners remain supportive in the current political and economic context in the Middle East and North Africa.

Currency devaluation exacerbates government fiscal challenges

The large devaluation of the pound puts upward pressure on public spending as the government offsets the impact of higher domestic prices and rising interest rates on households given low per capita incomes. The Central Bank of Egypt raised its main operation rate by 800 basis points since end-2023 to 27.75%.

More restrictive monetary policy in response to rising inflation could weigh on the government’s net interest burden, projected at more than 70% of revenue, and wide fiscal deficits expected at above 10% of GDP on average until 2028.

Servicing foreign-currency denominated debt, accounting already for more than 40% of central government debt as of Q2 2023, will be more expensive too. This will test the government’s ability to maintain a recent record of running a primary budget surplus, which averaged more than 1% of GDP between 2019 and 2023, as mobilising domestic resources will take time.

Budget balances could be supported by higher foreign tax receipts once converted to local currency and Egypt’s commitment to scaling down mega infrastructure projects as well as reducing off-budget capital expenditure. Still, these options contrast with current plans by the authorities studying costly further widening of the Suez Canal.

Beneficial as recently-announced international financial support and the exchange rate devaluation are for easing external-sector stress, the uncertainties surrounding further reform and the difficult policy trade-offs required moving ahead explain why we affirmed at this stage Egypt’s B- long-term credit ratings and maintained a Negative Outlook on 1 March 2024.

Access all Scope rating & research reports on ScopeOne, Scope’s digital marketplace, which includes API solutions for Credit Sphere, providing institutional clients access to Scope’s growing number of corporate, bank, sovereign and public sector ratings.

Thomas Gillet

Analyst

Alvise Lennkh-Yunus

Team leader

Matthew Curtin

Press contact